Medical Devices

The perfect hideout?

This week's blog post focuses on four medical device companies: Coloplast, Stryker, Boston Scientific, and Medtronic. Though these companies are in the same sector, they differ in their product focus - from chronic care to surgical innovations - and their approaches to global healthcare challenges. However, before we delve into these companies, we have to get a handle on Trump’s tariffs. The potential Trumpcession has become the backdrop that every investing decision falls in front of.

Visibility vacuum

Despite President Trump's 90-day pause on reciprocal tariffs, several trade levies remain in place, reflecting the administration's protectionist trade policies. These include:

1. A blanket 10% tariff on all imports into the U.S.

2. 25% tariff on imported steel and aluminum products from all countries.

3. Imported cars, including automobile parts, face a 25% tariff.

4. Goods from Canada and Mexico are subject to a 25% tariff unless they comply with USMCA provisions.

Furthermore, the US and China are now in a de facto trade war that will inflict economic harm to both nations and cause collateral damage globally. In the United States, tariffs will raise manufacturing costs, increase consumer prices, and hurt industries like agriculture, where soybean farmers are especially vulnerable. China faces slower economic growth and industrial output as it grapples with reduced US exports. Globally, the trade war can disrupt supply chains, forcing companies to relocate operations to other countries, which could introduce new inefficiencies and vulnerabilities. Developing nations reliant on exports to the U.S. and China are particularly affected, as they face declining demand and economic uncertainty.

The widespread tariffs have introduced significant uncertainty into corporate earnings, making it increasingly challenging for investors to evaluate companies. By raising manufacturing costs, disrupting supply chains, and shifting consumer demand, tariffs force businesses to adjust their strategies and financial forecasts. This unpredictable environment complicates long-term planning and investment decisions as companies struggle with the instability of global trade policies. Adding to the complexity, market volatility, currency fluctuations, and waning investor confidence further obscure earnings projections. This creates a feedback loop where business uncertainty fuels boardroom hesitation, perpetuating an environment of unpredictability that hampers strategic decision-making.

Despite the U.S. market closing higher last week, the economy remains under recession watch. While medical device companies are more insulated from short-term demand disruptions than industrial manufacturers, they are not immune to broader economic pressures. Historical data shows that even these relatively stable businesses face challenges, such as rising costs, supply chain disruptions, and delayed capital spending cycles during downturns. Investors should, therefore, disregard short-term guidance, which is often overvalued in volatile times, and instead prioritize evaluating long-term trajectories—such as compounded average revenue growth, EBIT margins, and sustainable earnings potential. This approach provides a clearer picture of a company’s resilience and strategic adaptability in uncertain economic conditions.

Coloplast

COLO specializes in intimate healthcare exigencies, producing medical devices for ostomy care, continence care, interventional urology, advanced wound care, and voice/respiratory care. The Danish company pays a dividend, yielding 3,3%, and has a market capitalization of DKK 157B.

In 2020, COLO introduced its "Strive25" strategy, targeting 8-10% organic revenue growth yearly and an EBIT margin exceeding 30% beyond 2024/25. This ambitious plan is underpinned by consistent investments in innovation, strategic acquisitions, divestments of non-core product categories, geographic expansion, and a user-focused commercial model designed to engage healthcare professionals and end-users.

COLO has fulfilled many of its non-financial goals under “Strive25”. Consistent innovation has resulted in the launch of new products like the male catheter Luja and the SenSura Mio portfolio, which have received positive market feedback and are driving growth in Continence Care and Ostomy Care segments.

Recent acquisitions, including Kerecis, Atos Medical, and Intibia, have bolstered its portfolio across Chronic Care, Voice and Respiratory Care, Advanced Wound Care, and Interventional Urology.

COLO’s building of manufacturing facilities in Portugal and Costa Rica supports geographical expansion outside of Europe as products like Luja and SenSura Mio get launched worldwide.

COLO has achieved an organic revenue growth of approximately 8%, reflecting the success of its strategic initiatives. However, the company has yet to meet its target EBIT margin of over 30%, currently standing at 27-28%. The divestment of its Skin Care business has positively impacted profitability by enabling a sharper focus on core areas like Chronic Care and Advanced Wound Care, contributing to improved operational efficiency and margin enhancement. Most analysts believe COLO will achieve its profitability goals by 2028.

Stryker

SYK is recognized for its innovative solutions, such as remanufactured devices and collaborative product design with healthcare professionals. The company offers products across three segments: Orthopedics (joint replacements), MedSurg (surgical equipment and patient handling), and Neurotechnology & Spine (devices for brain/spine surgeries and stroke treatment). The Michigan company pays a dividend with a yield of 0,9% and has a market capitalization of $133,7B.

SYK’s success in orthopedic robotics stems from its Mako SmartRobotics platform, which drives robotic system placements and proprietary implant sales. By integrating advanced robotics with its exclusive implants (e.g., Stryker knees), SYK has created a synergistic model that enhances surgical precision and patient outcomes while locking in demand for its artificial knees. This dual advantage has allowed SYK to outpace and “kneecap” competitors like Zimmer Biomet and Johnson & Johnson, solidifying its market leadership and fueling sustained growth.

Beyond its Mako platform, Stryker's growth is driven by several other strategic factors. Principally, SYK benefits from rising procedural volumes driven by favorable demographics, increased adoption of advanced technologies, and robust patient activity. SYK has seen strong growth in knee replacements, hips, extremities, trauma, and sports medicine.

Secondly, SYK continues to innovate with transformative products such as the Pangea Plating System and LIFEPAK 35 monitor/defibrillator. These launches enhance its portfolio across MedSurg, Neurotechnology, and Orthopedics segments.

Finally, SYK is a serial acquirer and has completed over 50 deals in the past decade. Recent acquisitions, including Care.AI, Nico Corporation, and Vertos Medical, are expected to contribute $300 million in sales in 2025. The latest acquisitions expand SYK's capabilities in virtual workflows, brain tumor removal tools, and chronic back pain treatments.

SYK hasn’t stated the same long-term financial goals as COLO. Regardless, the two companies have about the same compounded average revenue growth rate of around 8%. SYK’s management guides an organic revenue growth between 8-9% this fiscal year.

Boston Scientific

BSX focuses on minimally invasive medical devices for cardiology (e.g., stents), electrophysiology, endoscopy, urology, neuromodulation (pain management), and oncology. It specializes in life-saving technologies like pacemakers and defibrillators. The company is heavily involved in advancing treatments for chronic diseases through innovative devices. BSX doesn’t pay dividends and has a market capitalization of $138.54B.

BSX is, in my opinion, the most innovative company in the group. The company has a history of breakthrough innovations, from its early steerable catheters to the Taxus drug-eluting stent, which revolutionized coronary artery treatment. Recent standout technologies include the Watchman device for stroke prevention and the Farapulse Pulsed Field Ablation system for atrial fibrillation. These advancements highlight BSX's commitment to addressing unmet medical needs and maintaining its leadership in MedTech.

Besides innovation, strategic acquisitions have been a growth driver, expanding the product portfolio. In total, BSX has spent over $17B on buying companies over the last decade. The company has strived to drive operational efficiency and maintain strong gross profit margins (68.4% in 2024). This focus on efficiency supports reinvestment into R&D and strategic initiatives. In recent years, the company has also succeeded in breaking into emerging markets, particularly China, Japan, and EMEA regions. Investments in these regions have broadened its customer base and diversified revenue streams.

BSX forecasts revenue growth between 12.5% and 14.5% for the fiscal year 2025, driven by strong demand, especially for the Watchman and Farapulse systems. The company expects an EBIT margin in the high 20s, comparable to peers like COLO and SYK. However, BSX strives to reach an EBIT margin above 30%, just like COLO.

Medtronic

MDT is one of the largest medical device companies globally, offering products for cardiovascular health (pacemakers), diabetes management (insulin pumps), neurology (spinal implants), and surgical technologies. The company pays a dividend of 3,3% and has a market capitalization of $106.32B.

MDT is the slowest grower among these four companies. The company has struggled to keep up the same innovative pace as SYK and BSX. Furthermore, MDT’s acquisition strategy has been less aggressive and accretive to the bottom line. In addition, MDT has faced regulatory challenges in its diabetes pump business in the US.

In February 2025, activist investor Starboard Value revealed a significant stake in Medtronic (MDT). Renowned for its ability to enhance profitability and operational efficiency in the companies it invests in, Starboard's involvement often signals potential value creation, and it can be a good idea for other investors to ride on its coattails.

There has been significant speculation about MDT divesting less profitable parts of its business. Earlier this year, many expected the company to sell its Patient Monitoring and Respiratory Interventions (PMRI) segment, which generates $2.2 billion annually. However, Medtronic unexpectedly reversed course, citing stronger-than-anticipated performance in this segment. Instead of a sale, the company discontinued its ventilator product line while reorganizing the PMRI segment into a new unit called Acute Care and Monitoring (ACM). Maybe Starboard can speed up the divestment of non-core products in MDT’s portfolio and refocus the company around its most profitable parts.

Of course, companies can’t only rely on divestments to achieve higher profitability. Thus, MDT needs to launch new products that sell well, and to accomplish this, the company must spend more funds on R&D and innovations. MDT puts a lot of stock into its new HUGO Robotic Platform and advanced heart surgery devices to maintain competitiveness. More initiatives like these are something to be asked for among its investors.

MDT is expected to grow around 4% on the topline for the next fiscal year. EBIT margin is also expedited to be a few percentage points below COLO, SYK, and BSX.

The perfect hideout?

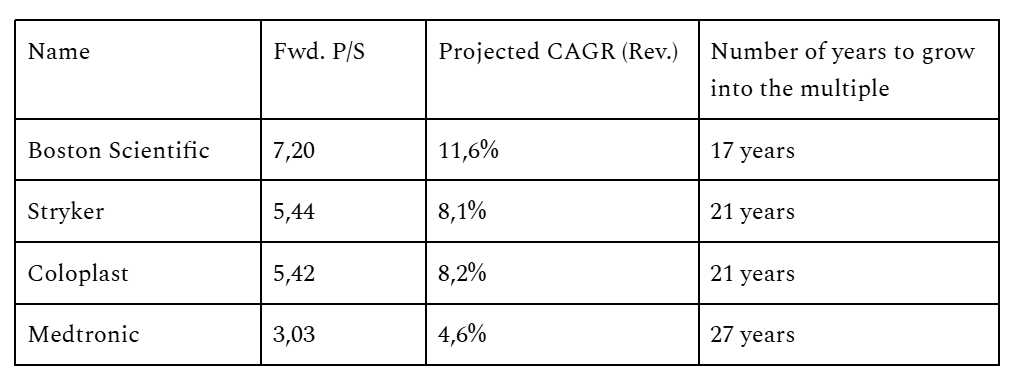

Medical devices can be a good hideout during these volatile times. The problem is that neither of the companies is cheap; see table below. The price/sales ratio will compress more than this in recessions. So, even though this sector can be viewed as recession-proof, don’t expect to escape unscathed from a bear market.

In the table above, I have taken the forward price/sales ratio and the projected average revenue growth rate for the next 5 years to calculate how long it would take for the companies to grow into their sales. Based on the calculation, although Boston Scientific is the most expensive company based on the price/sales ratio, it is the cheapest when we factor in the growth rate. The big question is whether Boston can keep on growing much faster than its peers.

We also see that the cheapest company based on the sales/price ratio is the most expensive when we factor in the growth rate. That said, 20 years is a long period, and Medtronic has ample time to turn its growth trajectory upward.

Where to invest?

In conclusion, Boston Scientific stands out as the most compelling company in this group. While long-term growth risks remain, the company's relentless innovation and forward-thinking approach continue to generate excitement among investors. With a dynamic product pipeline and a focus on cutting-edge medical technologies, Boston Scientific is well-positioned to sustain its momentum and deliver strong returns.

Stryker also presents an attractive investment opportunity for those seeking exposure to robotics and advanced surgical technologies. Coloplast's inconsistent growth trajectory raises concerns. The company's historical performance has been marked by volatility, with growth occurring sporadically rather than steadily, making it less appealing for long-term investors. Thus, I would put less trust in my projections regarding Coloplast versus the other companies in this assembly.

Medtronic remains an intriguing choice for value and dividend-focused investors. Starboard Value’s entrance offers a potential catalyst for revitalizing the company’s focus on growth and profitability. With strategic adjustments, Medtronic can unlock shareholder value over time.

Disclaimer: Important Information for Retail Investors

The information in this blog is for educational purposes only, not financial advice. Investing in stocks carries risks; past performance doesn't guarantee future results. Conduct thorough research and seek advice from financial professionals before investing.

The author is a retail investor, not a licensed advisor. Due to changing market conditions, content accuracy isn't guaranteed. All investments have risks, including the potential loss of principal. Assess your risk tolerance and goals before investing; diversification is key to managing risk.

The author may have positions in the mentioned stocks, which can change without notice. Readers should do their due diligence and consult professionals before acting on blog information.

Before investing, verify information from credible sources, understand prospectuses and financial statements, be aware of your financial situation, and consult professionals for aligned investment choices.

Readers are responsible for their investment decisions; the author is not liable for any outcomes. Investing in individual stocks carries risks; caution, research, and professional guidance are advised for informed decisions.