Cybersecurity

Cybersecurity

Are there any good investments in the sector?

Preamble

There are three things that are certain here in life: death, taxes, and cyber attacks. Furthermore, it is evident that the amalgamation of cloud computing and artificial intelligence (AI) presents a formidable challenge to enterprise cybersecurity. While transitioning to the cloud does not inherently render IT infrastructure less secure, it fundamentally alters the strategic landscape for network professionals, as the cloud significantly expands the potential attack surface.

AI introduces the prospect of early attack detection and expedited mitigation of their consequences, but concurrently, it opens avenues for larger, more potent, and intricately orchestrated cyber assaults. Regrettably, as investors, it is imperative that we acknowledge this sector's significance, for whether we embrace it or not, it is poised for rapid and substantial growth in the foreseeable future.

Introduction

Palo Alto Networks stands out as the dominant force in this particular market segment. It is my belief that delving into an in-depth analysis of this company would offer limited value, as it has been exhaustively scrutinized by numerous analysts within the equity sphere. Instead, I will provide a cursory examination of three alternative companies that may not have garnered as much attention: Crowdstrike (CRWD), Zscaler (ZS), and Okta (OKTA). In my view, these three enterprises merit an inclusion on your watchlist.

Crowdstrike

CRWD can be likened to antivirus (zero breach). Its core mission revolves around the proactive detection of potential threats at the network's periphery, known as endpoint security, and subsequently preventing these threats from breaching the network. Moreover, in the event of a breach, CRWD's software promptly notifies network specialists, enabling swift mitigation measures.

CRWD delivers its software through a cloud-based framework, aptly named the Falcon platform. This platform empowers network specialists to engage in real-time monitoring of cyber traffic, granting them insight into its response to potential cyber threats.

What sets the Falcon platform apart from conventional "antivirus" products? Much like other successful software ecosystems, its efficacy is driven by network effects. The platform's value increases as its user base expands. CRWD aggregates data pertaining to all cyber attacks across monitored endpoints, continuously fortifying its security defenses for all Falcon platform users. Furthermore, the company employs machine learning models for ongoing threat detection in the ever-evolving cyberspace, enhancing network security for all its users. Notably, it is the network effects and rapid growth that render this an intriguing long-term investment opportunity.

The Falcon platform operates on a subscription-based model, aligning with the prevalent Software as a Service (SaaS) paradigm. The sustained retention of subscribers underscores the platform's enduring appeal and its ability to maintain customer loyalty.

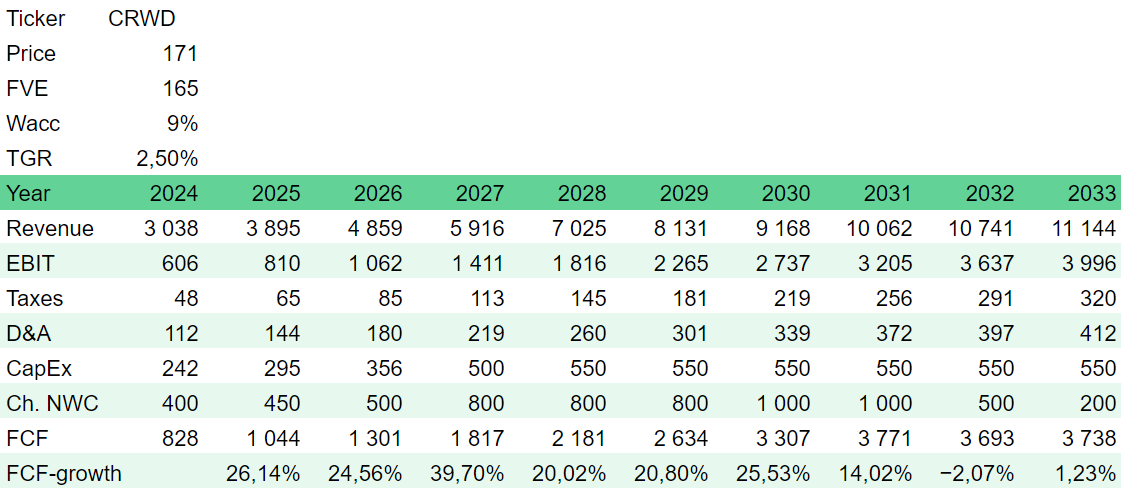

Valuation

CRWD trades on a free cash flow yield of just under 3,5 % for this fiscal year. I have estimated a fair value of the company of around $165 which means that the market gives the stock a fair price right now, as you can see from the table below.

However, it is worth noting that the stock price is highly volatile.

Share price volatility

As evident from the chart provided below, the stock exhibits notable volatility. Consequently, long-term investors should prepare themselves for a turbulent journey, characterized by substantial downturns and rapid surges in value.

In this context, strategic market observation becomes imperative for making well-timed entry decisions. Over an extended period of scrutiny, I have observed that this particular stock demonstrates heightened price sensitivity to both misses and beats during reporting periods. For individuals contemplating a long-term investment in this stock, I would recommend considering acquisition during periods of market weakness rather than when it is riding high.

It is important to recognize that, like all growth stocks, there exists a degree of uncertainty regarding the continuity of its growth trajectory. Nonetheless, I hold the belief that Crowdstrike's value proposition within the cybersecurity sector remains robust, offering an extended runway for growth. Given the right entry point, this investment opportunity presents considerable appeal.

Zscaler

Zscaler goes one step further than Crowdstrike, even though it works under the same paradigm, never thrust, always verify (zero thrust). So, the core mission of ZS software is to stop any nefarious breaches from propagating within the network by securing all connections within it. The Zscaler Zero Trust Exchange platform empowers customers to secure and interconnect users, workloads, and IoT/OT devices, fulfilling two overarching functions: Zscaler Internet Access, facilitating secure access to external applications, and Zscaler Private Access, facilitating secure access to internal applications.

Notably, ZS's architecture stands in stark contrast to the conventional "hub-and-spoke" corporate network model, where traffic from branch offices is routed to centralized data centers for security inspections and policy enforcement before reaching its destination.

In contrast, Zscaler's Zero Trust Exchange platform functions as an intelligent switchboard, employing business policies to establish secure connections among users, devices, and applications across any network, while concurrently providing robust safeguards against cyber threats and data loss. This approach eliminates the need for organizations to procure and manage a diverse array of high-cost appliances, a task that typically demands a substantial pool of highly skilled security personnel, which can be both costly and increasingly challenging to find.

Thus, ZS offers a product that seamlessly aligns with a cloud-centric framework, driving cost efficiencies for users while fortifying network security across various industry verticals. Much like Crowdstrike, Zscaler's business model revolves around a subscription-based service, and the platform's value escalates in tandem with its expanding user base, thereby enabling ZS to allocate greater resources toward enhancing the platform's security features.

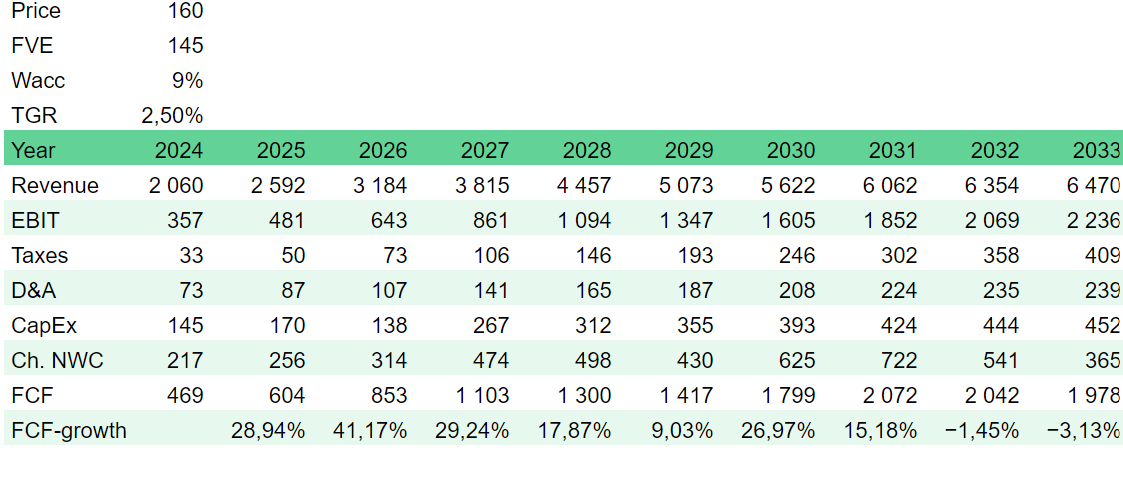

Valuation

ZS trades on a free cash flow yield of around 3 % for this fiscal year. According to my DCF valuation, ZS is slightly overvalued here, as shown below:

Share price volatility

Just like CRWD, ZS is a somewhat volatile stock. From the chart below, we can see that ZS went through a substantial price appreciation during the COVID-19 pandemic. After being rerated under the tech bear market last year, it has now steadily been climbing upwards.

Zscaler is an interesting investment, but the same goes for ZS as CRWD, for long-term investors it is imperative to find an adequate entry point. In my assessment, an entry point below $150 holds promise as a sound investment, contingent upon the company's ability to execute its strategic plans. In any case, if you invest in this stock be prepared for a wild ride.

Okta

Okta is involved in access management. Every security specialist knows that networks need to be sliced, diced, segmented, and partitioned. In short, good networks are built on a need-to-know basis from the core to the periphery. Access to the entire technology stack and business logic should be limited to a select portion of the workforce. The primary objective is to safeguard the overall network integrity and prevent the proliferation of malicious activities throughout the system.

Okta offers its clients a comprehensive, ready-to-use platform for efficient identity management across their entire network. Organizations employ Okta to securely access a diverse array of cloud, mobile, and web applications, on-premises servers, application programming interfaces (APIs), IT infrastructure providers, and services, all accessible from a wide range of devices. Developers leverage Okta's platform to securely and seamlessly integrate identity functions into the software they develop, enabling them to concentrate on their core mission.

Employees and contractors utilize the Okta Identity Cloud to conveniently and securely access the applications necessary for their most critical tasks. Additionally, organizations rely on Okta's platform to collaborate with their partners and enhance customer interactions with more contemporary and secure cloud and mobile experiences.

Similar to CRWD and ZS, Okta operates on a subscription-based model to deliver its services.

Valuation

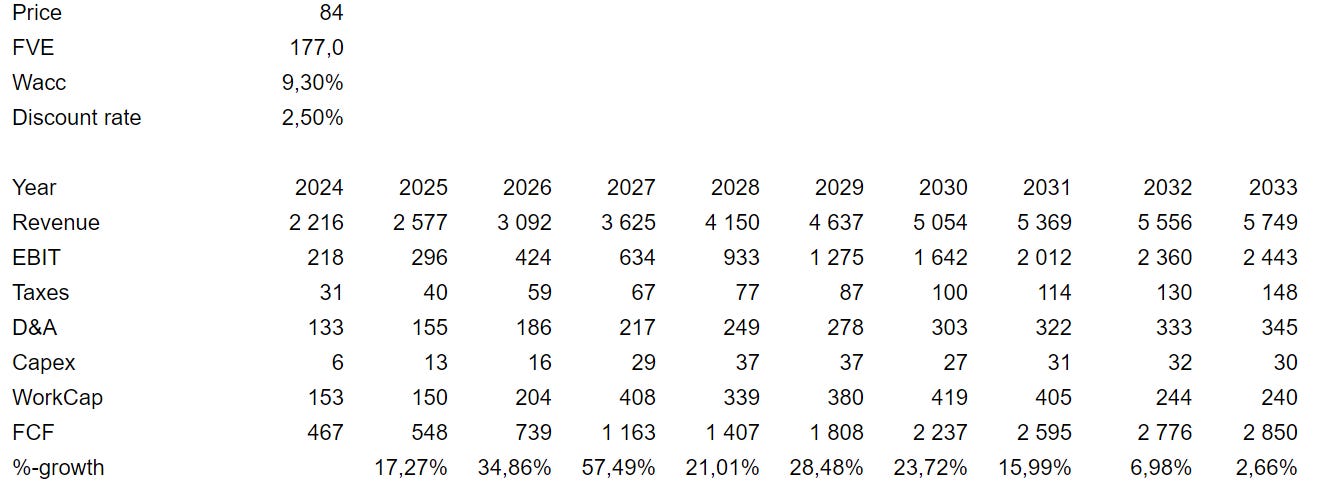

Okta is the only company that is undervalued according to my discount cash flow analysis, see below.

Nonetheless, the prevailing low stock prices of the company may be indicative of underlying factors. I remain uncertain about the extent of the value that Okta contributes to corporate environments where proficient cybersecurity teams diligently monitor network segmentation and access, both internally and externally. Nevertheless, it is essential to acknowledge that access management represents a pivotal facet of cybersecurity. It is plausible that Okta's mission may be tailored to serve smaller businesses with limited resources allocated to network management. In light of this, my assessments could potentially be biased.

It is worth noting that small businesses constitute a significant portion of global economies, a fact exemplified by Intuit's prosperous focus on catering exclusively to small and medium-sized enterprises. Should Okta successfully retain its clientele and sustain its recent growth trajectory, the Okta Identity Cloud platform could emerge as a highly valuable asset.

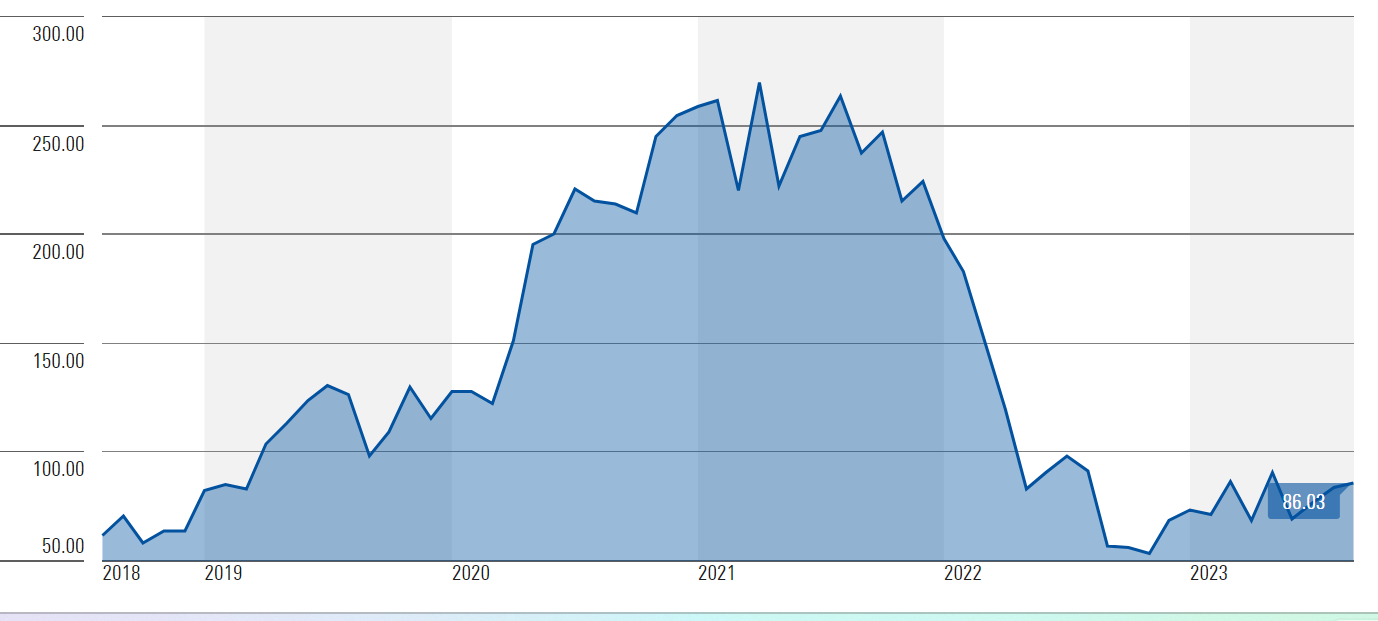

Share price volatility

Okta experienced significant growth during the COVID-19 pandemic, as evidenced by the fivefold increase in its share price, as depicted in the table below. However, in the spring of 2022, the stock encountered a substantial decline. It's noteworthy that this decline cannot be solely attributed to the broader disfavor towards tech stocks. Okta faced considerable scrutiny in the media due to challenges in executing its fundamental mission: ensuring secure access management. Recent developments indicate that these issues have largely been resolved, and Okta now operates with reduced negative sentiment surrounding its name. In the most recent quarterly report, the company surpassed Wall Street's expectations in terms of both revenues and earnings, contributing to a modest uptrend in the stock's performance this year.

Personally, I maintain some reservations regarding investment in this stock. As mentioned earlier, my perspective may contain some bias. While the current stock price appears quite attractive, so it must be other factors that deter investors from considering this equity. For proactive investors, one approach could involve initiating a small position and building on it if Okta consistently demonstrates improved execution in the future.

Conclusion

This three-stock rundown shows that investing isn’t easy. I’ve got two holds and one maybe. In any case, this is an interesting sector that one should keep an eye on, and companies within this space are violently volatile despite the fact that many of them grow exponentially. For attentive market observers, it should, therefore, be possible to find attractive entry prices in the future.

Disclaimer: Important Information for Retail Investors

The information provided in this blog is intended for educational and informational purposes only and should not be construed as financial advice or a recommendation to buy, sell, or hold any securities. Investing in individual stocks involves inherent risks, and past performance is not indicative of future results. Before making any investment decisions, it is crucial to conduct thorough research and consider seeking advice from qualified financial professionals.

The author of this blog is a retail investor and not a licensed financial advisor or registered investment professional. While the author strives to present accurate and up-to-date information, there is no guarantee that the content provided is accurate, complete, or current. Market conditions can change rapidly, and stock prices can be volatile.

All investments carry a degree of risk, including the potential loss of principal. Retail investors should carefully assess their risk tolerance and investment goals before making any investment decisions. Diversification is a key strategy to manage risk, and investing solely in individual stocks may expose investors to higher levels of risk compared to a diversified portfolio.

The author may have positions in the stocks mentioned in the blog. These positions may change at any time, and the author is under no obligation to update readers on such changes. It is recommended that readers do their own due diligence and consider seeking advice from qualified professionals before acting on any information presented in this blog.

Investors should be aware of the inherent limitations of the information available on the internet, including the potential for misinformation and bias. Always verify information from credible sources and cross-reference any data presented in this blog.

In accordance with prudent compliance, the author encourages readers to carefully review and understand the prospectuses, annual reports, financial statements, and other relevant information before making investment decisions. Retail investors should be aware of their own financial situation and consult with appropriate professionals to ensure that their investment choices align with their individual circumstances and goals.

By accessing and using this blog, readers acknowledge and agree that they are responsible for their own investment decisions and any outcomes that may result. The author and any related parties are not liable for any losses, damages, or actions arising from the use of the information provided in this blog.

In conclusion, investing in individual stocks carries risks that may not be suitable for all investors. Retail investors are advised to exercise caution, conduct thorough research, and consider seeking guidance from qualified financial professionals to make informed investment decisions.