Artificial Intelligence: It Is All About The Data!

Can we make any good investments in cloud data storage?

Yes we can, the large cloud platforms offer storage in their data centers, including Google with BigQuery, Amazon with Redshift, and Microsoft with Azure Synapse Analytics. It's indisputable that these industry giants have yielded favorable returns at various points in time.

However, our focus is not on the great conglomerate behemoths in the cloud business. Our emphasis is on evaluating smaller companies that specialize in various forms of cloud data storage. Besides specialization in storage, another prerequisite is that companies have the ability to support key processes central to the ongoing AI revolution to be included in this analysis.

Thus, this analysis centers on three key players: Snowflake (SNOW), MongoDB (MDB), and Pure Storage (PSTG).

Snowflake

SNOW is the first data platform built exclusively for cloud storage. The data platform can handle both structured and unstructured data, which can be stored in either data warehouses or data lakes. Snowflake went public in 2020, it has 5,900 employees, around 3,000 customers, and a market capitalization of about $50B.

Value proposition

Cloud storage effectively addresses numerous data management challenges that organizations have historically grappled with. Snowflake's data warehouse stands out by eliminating the need for hardware or software installation, setup, and maintenance. In fact, SNOW oversees the entire architecture, including stringent security requirements, providing a hassle-free experience for its users. Snowflake is renowned for delivering cost-effective services.

SNOW can be viewed as a normal Software as a Service (SaaS) company, except that its revenues are built on a consumption rather than a subscription model. Hence, customers pay only for the amount of data they store in Snowflakes DB. This consumption model offers unparalleled flexibility and scalability to users, particularly when they require extensive data for running AI models. When customers engage in AI model processing, the demand for storage increases proportionally. However, once these models complete their processes, the storage needs typically decrease. This elasticity in storage demands is exceptionally valuable from the perspective of artificial intelligence applications.

SNOW's data platform is characterized by its cloud-agnostic nature, enabling seamless compatibility with various cloud solutions. An appealing feature for many users is the dedicated User Interface (UI) it offers, providing an intuitive environment for executing queries through both button-based and click-based interactions. Particularly noteworthy from an artificial intelligence standpoint is SNOW's reputation for outstanding performance, boasting the industry's fastest query execution speeds. Additionally, users can effortlessly expand the capacity of their virtual warehouses to leverage additional compute resources, facilitating accelerated data loading and the execution of extensive query workloads.

AI configuration

A priori, SNOW’s data warehouses seem rigged for a revolution where data is the raw material that drives the whole thing. However, this doesn’t mean that SNOW doesn’t continue to configure its data platform for the AI revolution. Their dedicated framework, Snowpark, facilitates machine learning workflows, ensuring rapid data access and scalable processing through Python or SQL.

Moreover, SNOW's recent acquisitions—Neeva, Streamlit, and Applica—enhance its AI capabilities. Neeva bolsters search and query functions with AI, while Streamlit empowers developers to create applications based on large language models. Applica utilizes deep learning for data sorting, applicable across various data types. Its software can, for example, be used to search and sort data in large sets of documents.

Everything about this enhances SNOW’s value proposition. However, I think the most revolutionary part of Snowflake’s AI configuration is its creation of a synthetic data marketplace. In fact, real data comes with complications. In the healthcare industry, for example, there are privacy rules that hinder organizations from training AI models on patient data. The same issues might arise in several industries. Enterprises can’t just willy-nilly use customer data. It is here SNOW comes in, by using AI to create datasets that mimic real-world data, they can offer customers data that closely resembles what actually goes on in reality. This means businesses can train AI algorithms and perform tests and simulations without exposing private or sensitive information that might be contained in real-world data. SNOW has stated that its synthetic data marketplace will be one of its greatest sources of revenue growth going forward.

Finally, like many players in the technology industry, SNOW has partnered with Nvidia, leveraging NeMo LLM to create a platform enabling the development of generative AI applications like Chatbots and search engines, integrating seamlessly with Snowflake data. This strategic collaboration exemplifies SNOW's continuous efforts to advance AI solutions.

Valuation

In my view, SNOW is fairly valued here. Market consensus holds optimistic expectations for SNOW's top-line growth in the forthcoming years. While SNOW boasts a commendable product, sustaining a growth rate exceeding 30% over the next three years can pose challenges. Nevertheless, the company's growth prospects remain promising. It is imperative to note that SNOW is highly sensitive to changes in interest rates from a valuation perspective.

I have applied a discount factor of 10% to SNOW's valuation, considering an equity risk premium of 5%, an interest rate of 4.5% (based on the 10-year treasury bond), and a 0.5% dilution risk. It is worth mentioning that you have the flexibility to adjust the discount factor if you deem it appropriate. SNOW's beta stands at 0.8. Notably, a 1% increase in interest rates translates to a decrease of approximately $25 in the fair value estimation according to my discounted cash flow (DCF) analysis, see below.

MongoDB

MongoDB is a document-oriented DB designed to empower users with the capability to store vast amounts of unstructured data, falling under the category of NoSQL databases. MDB offers a comprehensive ecosystem around its DBs, encompassing managed services, an integrated development environment (IDE), analytics tools, and search functionality. Within this environment, users can retrieve data from the documents based on specific keys and their associated values.

MongoDB's document-oriented DBs integrate with all major programming languages, making it highly versatile. The company has around 33,000 customers, over 4,600 employees, and a market capitalization of close to $25B.

Our primary focus here lies in evaluating MongoDB's cloud data platform, known as Atlas, which occupies a central position in the company's strategic initiatives, particularly in the realm of AI.

Atlas - the jewel in the crown

It is the cloud data platform that is responsible for MDB’s stellar growth in the last few years. Today Atlas represents 50% of the company’s revenues. Similar to Snowflake, MongoDB’s software is cloud-agnostic, allowing users the flexibility to select their preferred cloud platform for deployment. MDB assumes the responsibility of managing the data platform, enabling users to focus entirely on their operations.

While Snowflake primarily caters to the requirements of data scientists, MDB centers its offerings around the needs of software developers. Unlike Snowflake, MongoDB does not provide data warehouses to its users. MDB contends that developers can effectively meet their needs with databases, as its databases offer most of the analytical capabilities required by developers. However, MDB has just recently launched MongoDB Atlas data lakes in order to serve the needs of users who want to venture into the world of machine learning and predictive analytics.

MDB also adopts a slightly distinct revenue model. Its payment plans are subscription-based and come with limitations on the amount of data that can be stored, making it less flexible from a user perspective compared to SNOW’s offerings.

MongoDB’s AI initiatives

MDB has taken several initiatives to come on the front foot in advance of the AI revolution. This summer, MDB launched MongoDB Atlas Vector Search to simplify the development of AI language and generative AI applications. The vector capability is hard to explain but functions as a framework that defines the relationship between words, which serves to help generative language models organize themselves internally, ultimately producing meaningful results. Alas, the new capability allows vectors embedded directly in data stored.

MDB likes to call itself the go-to platform for developers and is continuously innovating to reduce friction in the software development process From an AI perspective, MDB's support for Kotlin and Python is crucial. For instance, the PyMongoArrow library empowers developers to seamlessly convert MDB-stored data using popular Python-based analytics frameworks. Recognizing the increasing fusion of operations (databases) and analytics (data warehouses and lakes), MDB meets the demands of AI application developers by partnering with industry leaders like Databricks, Apache Spark, and MindsDB. These collaborations transform Mongo's DBs into potent tools for predictive analysis.

Finally, acknowledging that AI application development requires a dedicated commitment, MDB has introduced the MongoDB AI Innovators Program. This initiative demonstrates MDB's serious approach to AI by providing incentives and support to developers engaged in creating AI applications. Through this program, developers receive credits to foster their projects within MDB's ecosystem, underscoring MongoDB's dedication to nurturing innovation and excellence in the realm of artificial intelligence.

Valuation

MongoDB has consistently surpassed market expectations in its quarterly reports, showcasing a remarkable track record. The company's revenue has surged by a factor of eight since 2018, a testament to its robust performance. According to Wall Street consensus, MongoDB is anticipated to sustain its growth momentum, with the top line projected to expand by 25-30% over the next three years. While this growth outlook is slightly more moderate than SNOW's estimates, which exceed 30%, it still represents a substantial rise.

The pivotal question that arises, as always, is whether MDB can maintain this impressive trajectory. It is noteworthy, however, that despite the impressive revenue growth, MDB is not expected to achieve net income positivity on a GAAP basis until 2027/28. Based on my DCF analyses, I have assessed MDB to be slightly undervalued here, underscoring the potential inherent in its current market valuation, see below.

Pure Storage

PSTG is certainly part of the AI revolution, just like SNOW, MDB, Alphabet, Microsoft, and Amazon, even though it receives less attention and operates in parts of the market that might be viewed as less glamorous. The company specializes in the development and provision of all-flash data storage products and solutions tailored for modern data centers. Pure Storage has around 5,400 employees and a market capitalization of just above $11B.

So what is flash storage? To demystify the technology, flash storage, akin to the flash memory sticks found in smartphones, offers a more compact alternative to spinning disks normally used for data storage. In contrast to disks, flash memory has no moving parts. Although spinning disks continue to be prevalent in data centers where space constraints are less critical, flash storage has also gained traction here due to its superior attributes. While historically considered pricier than traditional disk storage, the cost disparity has diminished over time, making flash storage increasingly viable for data center applications. PSTG stands at the forefront of this shift.

In essence, flash-based storage delivers significantly enhanced performance when compared to spinning disks, offering faster data access times, lower latency, and higher throughput, thereby revolutionizing the efficiency and responsiveness of modern data centers.

How does PSTG make money?

Pure Storage sells both hardware and software solutions. Software revenues are in large part centered upon a traditional SaaS model with recurring subscription income. Subscription service revenues are only ⅓ of the total revenues but are at the same time the fastest growing part of the business.

In the realm of hardware, PSTG’s success is underpinned by the advanced QLC NAND flash storage architecture, a technology that marries performance, capacity, and cost-effectiveness. This innovative approach has positioned QLC NAND as the leading solution for data storage in the contemporary landscape. Notably, PSTG’s recent launch of the Flashblade series leverages the strengths of QLC Flash and Pure's pioneering architecture. These appliances are meticulously engineered for large consolidated data environments, making them a groundbreaking mainstream flash storage solution that surpasses the economics and performance of traditional hard disk drives. A key feature of FlashBlade is its exceptional energy efficiency, consuming only 20% of the electricity compared to conventional disk drives, thereby offering significant long-term cost savings to users.

PSTG subscription business is built on the same consumption model that powers Snowflake revenue streams. Users pay only for the storage they use. Pure Storage offers cloud storage services on Amazon Web Services (AWS) and Microsoft Azure. PSTG subscription services let users combine their need for secure storage of their data with the architecture PSTG is known for from its hardware side. The company boasts that it is one of the most economical choices in the marketplace.

Beyond storage, Pure Storage is dedicated to spearheading the modernization of enterprise IT across infrastructure, operations, and applications. PSTG offers an extensive ecosystem of software products, including Pure1, Purity, FlashArray File Service, and Pure Fusion, which in various ways assist customers in optimizing their data operations. Moreover, the Portworx software suite empowers cloud-native applications with comprehensive Kubernetes Data Services. Even more, is the configurations PSTG has undertaken to embrace AI.

PSTG embrace AI

FlashBlade is a cutting-edge product meticulously tailored to the demands of artificial intelligence, destined to meet the requirements of contemporary analytics and AI applications for the foreseeable future. Representing a significant advancement in handling unstructured data vital for AI, FlashBlade outshines its predecessors from PSTG by doubling the density, performance, and power efficiency.

This revamped architecture strategically disentangles storage and compute functions, paving the way for a remarkably adaptable and personalized file and object storage platform. This platform is meticulously designed to cater to a diverse range of analytics and AI workloads. FlashBlade adeptly manages everything from high-flash performance workloads to disk-based setups emphasizing hybrid density and efficiency.

Expanding on the capabilities of FlashBlade, Pure Storage has unveiled an AI-ready infrastructure referred to simply as AIRI. Hence, the company gets no points for being creative in the name department, technically though, the product is very impressive. AIRI is the outcome of a collaborative effort between Nvidia’s DGX systems and Pure Storage FlashBlade storage. This synergistic partnership ensures users have access to unparalleled computing and storage resources optimized for AI applications.

Additionally, it is noteworthy that PSTG has developed a comprehensive cloud solution in collaboration with VMware, aptly named FlashStack. This solution seamlessly integrates storage, compute, and network functionalities. However, the success of this recent launch is still unfolding and warrants keen observation. FlashStack is built on all of the technology known from AIRI.

Valuation

In my DCF analysis, PSTG is significantly undervalued, as indicated below.

The consensus estimates suggest modest expectations, with revenue growth projections hovering around 10% over the next three years. While the current hardware market faces potential challenges amid a downturn, Pure Storage boasts a robust product portfolio. Several compelling factors indicate a trajectory toward robust growth in the foreseeable future, albeit with anticipated occasional obstacles along the path.

Conclusion: to buy or not to buy

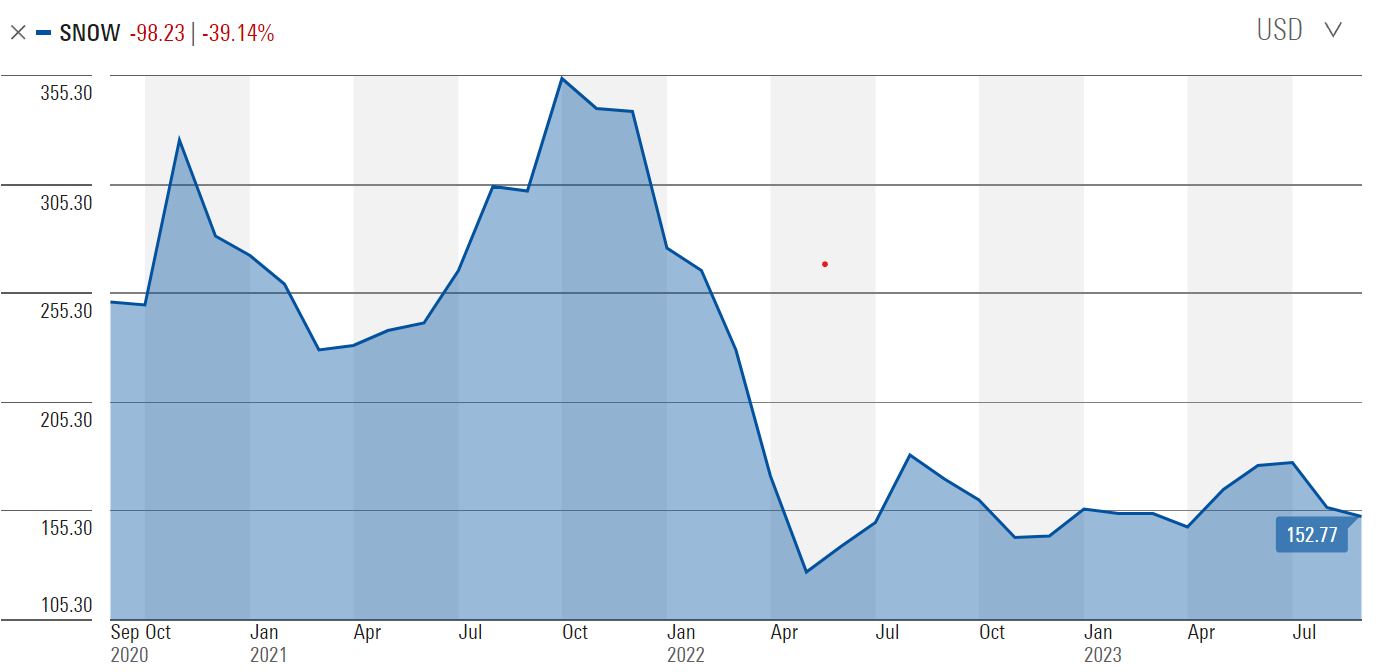

Snowflake - made its debut more or less during the Covid-19 pandemic and was an instant hit with investors. Now, market pricing is more constructive for investors wanting to get into a quality company that is perfectly positioned to take advantage of advances in AI. Obviously, AI is going to drive the need for data storage even higher than what we currently witness. However, investors should be aware of the fact that Wall Street has high hopes for growth in this market. If SNOW’s revenue growth falls under 30 % before 2027, Wall Street might push its estimates down. There is also big competition from Google, Amazon, and Microsoft. SNOW’s trump card is its state-of-the-art technology and multi-cloud capabilities. However, large cloud platforms have nearly an infinite amount of cash to invest in their business, so it is very hard to compete against them over time. Currently, SNOW is making an impressive claim on this market segment, and I contend that this will continue in the next 5 years. In conclusion, I rate SNOW as a weak buy here. SNOW’s share price can be studied in the chart below:

MongoDB - has pretty much made violent comebacks to the upside every time investors count the company out. Obviously, there is high competition in the database businesses. You have both structured and unstructured data, relational databases, and numerous schemas for NoSQL databases. MDB competes with all of these but has also carved out a position as the best document-oriented database. It has also carved out a narrow moat as the data platform for software developers. Mongo is also embracing AI enthusiastically. In conclusion, I rate MDB as a buy here. MDB’s share price can be examined in the chart below:

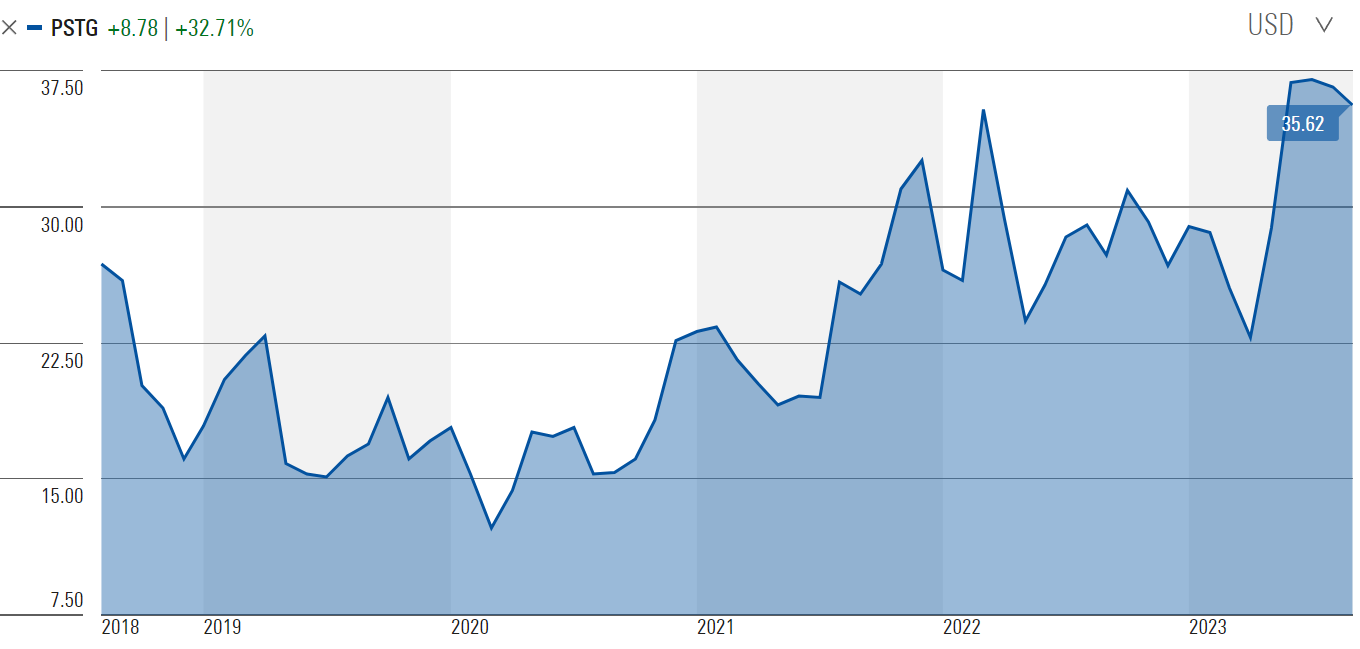

Pure Storage - comes in as clearly undervalued from a valuation perspective. PSTG has some competition from NetApp and Dell but the space it operates in doesn’t seem too crowded. Dell has gone even stronger than Pure Storage in the stock market this year. However, I think PSTG is an even better long-term pure play on storage and AI in the next decade. Dell has a more sprawling business to take care of. In conclusion; I rate PSTG as a strong buy here. If you do decide to buy shares in this business, as I have done, you could also impress people around you with the advantages of flash memory. In fact, they might get so impressed that they fall asleep. PSTG’s share price can be viewed below:

Disclaimer: Important Information for Retail Investors

The information provided in this blog is intended for educational and informational purposes only and should not be construed as financial advice or a recommendation to buy, sell, or hold any securities. Investing in individual stocks involves inherent risks, and past performance is not indicative of future results. Before making any investment decisions, it is crucial to conduct thorough research and consider seeking advice from qualified financial professionals.